Markel Stock Analysis & Deep Dive

Markel Stock Analysis & Deep Dive

What's the current status of the mini Berkshire Hathaway?

Intro

Markel is a company that has fascinated me for a long time and is often referred to as the mini-Berkshire Hathaway. After seeing Markel’s CEO Tom Gayner live in Omaha in early May, I can fully understand this reasoning. Tom Gayner is a very fascinating person and amazing speaker.

Watch this video to better understand the man behind Markel’s success.

History

It all started with a small insurance company for jitney buses.

Markel went public in 1986 at a price of 8,33$ per share and a market cap of 15m. I guess you would now love to make a call into the past and tell your parents to invest in this company. These 8,33$ compounded at an annual rate of 15% and turned this initial small amount to a share price of 1300$ and 17.4bn in market cap.

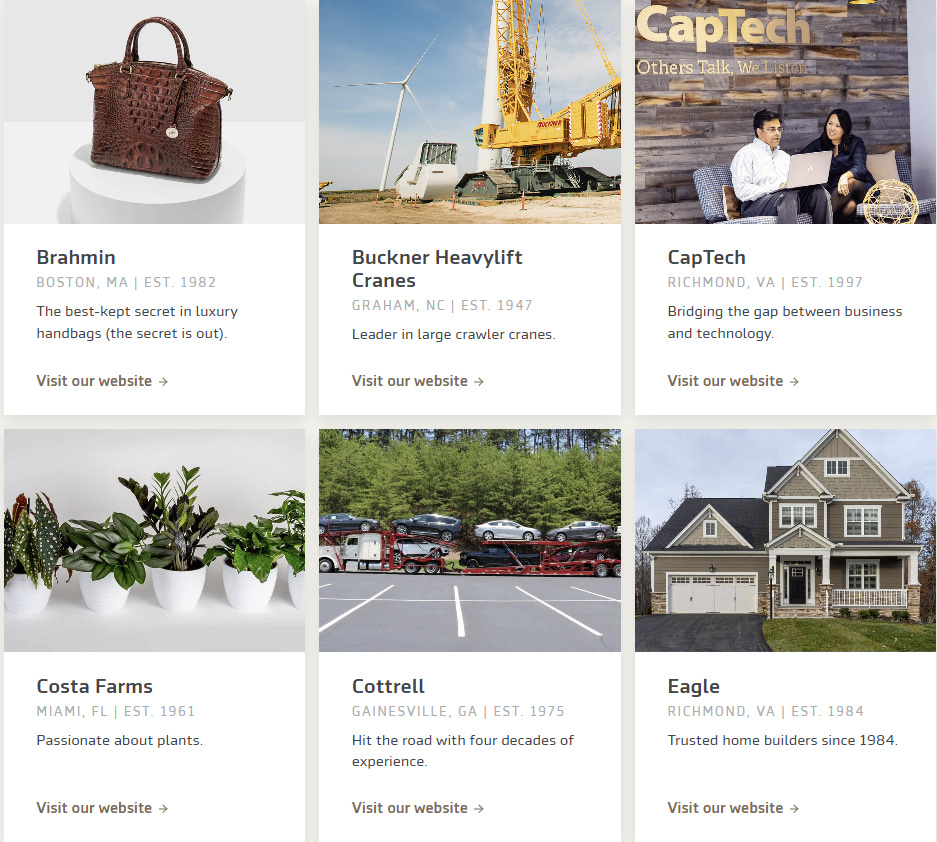

2005 marked a major milestone for Markel, when Markel bought the first non-insurance company in AMF Bakery Systems.

An overview of the businesses that Markel invested in can be found here:

https://www.mklgroup.com/what-we-do/markel-ventures

You will find everything from a luxury handbag producer, to a crane company and even a home builder.

Today Markel employs about 21000 people of which 5000 are working in the insurance business and 16000 within Markel Ventures.

Writing a deep dive takes me 40+ hours to get a proper understanding of the company and the attributes of the industry it is working in. You will support me a great deal if you a) subscribe to this substack and b) recommend this blog to your friends and family. To all existing subscribers: Thank you for your support! :)

Business Overview

Similar to Berkshire Hathaway, the backbone of Markel is the insurance business. The float from this insurance business is then used to fund other investments. The float is the money being payed upfront by the customers. Markel has a wide portfolio of holdings in stock listed companies as well as fully owned subsidiaries. This approach is modeled after the great Berkshire Hathaway (not the worst role model).

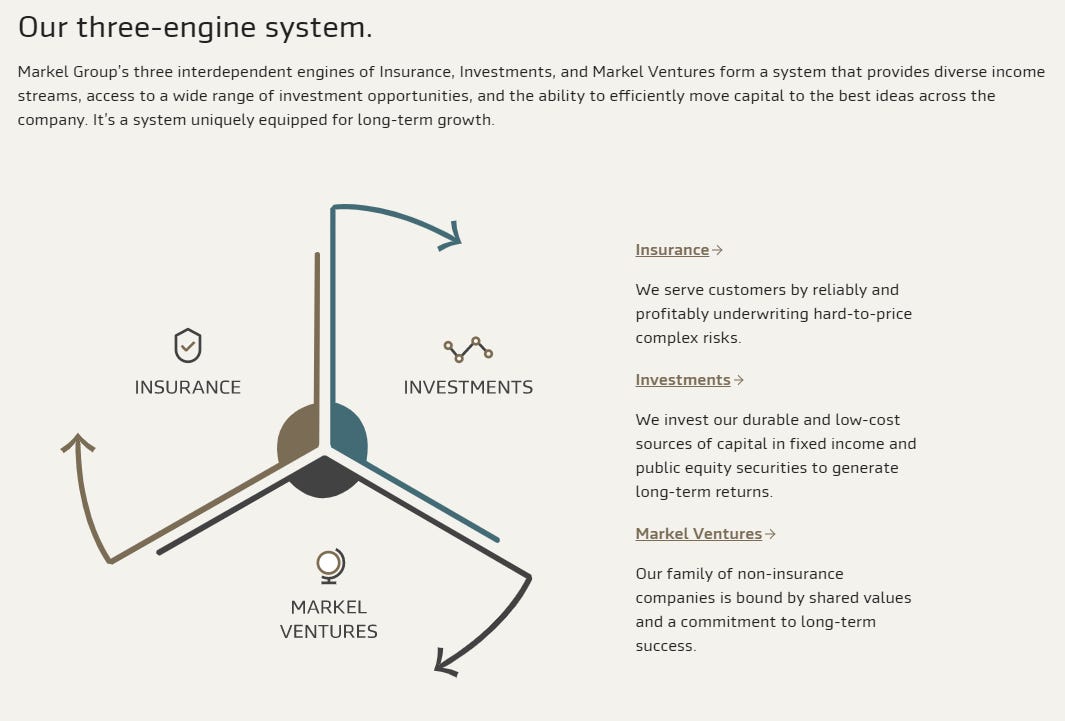

To understand Markel, it is important to separate it into 3 pillars:

Insurance business

Operating businesses

Security investments

Tom Gayner said the following on the release of the Q1/23 earnings:

"Markel Ventures achieved impressive organic revenue and profitability growth. In insurance, we continue to grow while maintaining our decades long approach to disciplined underwriting. Our investment income continues to benefit from higher interest rates, and we experienced favorable returns in our equity portfolio. As always, we encourage investors to focus on our operating performance over the long term, where our three-engine system continues to demonstrate strength, durability and profitable growth,"

“We believe our financial performance is most meaningfully measured over longer periods of time, which tends to mitigate the effects of short-term volatility and also aligns with the long-term perspective we apply to operating our businesses. We generally use five-year periods to measure our performance.”

This long-term thinking is exactly what I also apply in choosing my investments.

Insurance Business

Markel is a specialized insurer. Whereas in the standard market the insurance rates are highly regulated and have a high degree of predictability, specialty insurance is not so much about the price and more about the expertise and service of the provider. Hence higher rates can be achieved.

Taken from the annual report: Examples of niche insurance markets that we have targeted include liability coverage for highly specialized professionals, wind and earthquake-exposed commercial properties, equine-related risks, transaction-related risks, classic cars, credit and surety-related risks, collateral protection risks and marine, energy and environmental-related activities.

While Markel is a global companies, the absolute majority of premiums were written from the platforms in the US, UK, Germany and Bermuda. 80% of all gross premiums are allocated to risks or cedents based in the US.

While the public opinion on insurance companies expects a very stable market, the specialty insurance business experiences large fluctuations in the pricing. In times of excess underwriting capacity (e.g. due to high availability of capital) the conditions for insurers worsen. In times of tight capital, the insurers have favorable terms and can push for better rates. Since Markel is cautious about writing insurance policies which do not fulfill the profit targets,

As per Markels 10K report: The combined ratio is a measure of underwriting performance and represents the relationship of incurred losses, loss adjustment expenses and underwriting, acquisition and insurance expenses to earned premiums. A combined ratio less than 100% indicates an underwriting profit, while a combined ratio greater than 100% reflects an underwriting loss.

Investment Business

Policyholder funds are invested predominantly in high-quality government and municipal bonds and mortgage-backed securities that generally match the duration and currency of our loss reserves. Therefore the unrealized gains and losses on the fixed maturity securities do not matter in the long run.

“When purchasing equity securities, we seek to invest in profitable companies, with honest and talented management, that exhibit reinvestment opportunities and capital discipline, at reasonable prices. We intend to hold these equity investments over the long-term.”

This sounds a lot like the principles laid out by Warren Buffett and Charlie Munger and are also the principles by which I choose my investments.

Markel managed to outperform the S&P500 for more than three decades by now. One could say that they know what they are doing.

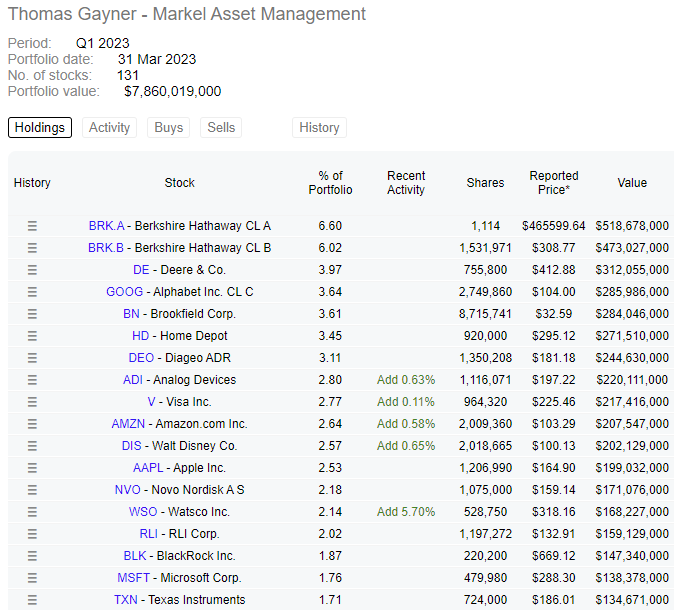

Luckily we can access Markels 13F filings and see which stocks are part of their portfolio. Most of these companies are outstanding investments and resemble the long-term investment approach taken by Markel.

Markel Ventures

In 2022, our Markel Ventures operations reported revenues of $4.8 billion, operating income of $325.2 million, net income to shareholders of $192.6 million and EBITDA of $506.3 million. Local management has autonomy in how to operate the business. That again is so similar to Berkshire Hathaway.

Business Performance

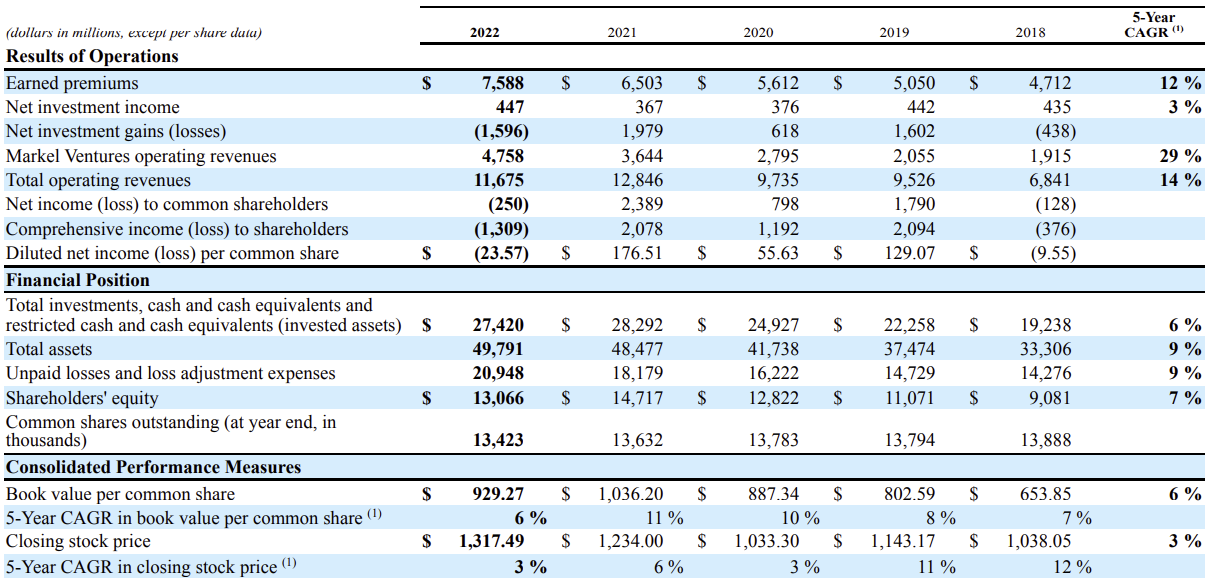

As you can see, the earned premiums from the insurance business have been growing steadily at a CAGR of 12% for the last 5 years. Markel Ventures operating revenue has been growing at a CAGR of 29%. The value of the total investments has been growing to 27bn at a CAGR of 6%.

While the book value per common share has been growing with a CAGR of 6%, the share price has been only growing at 3%.

Markel has shown a strong track record with their equity investments with a 5 year CAGR of 9.5% and a 10 year CAGR of 13.2%. The fixed maturity performance can be disregarded, since the rising interest rates had a strong impact on unrealized losses in 2022. Since Markel holds these investments to maturity, these effects are temporary.

Markel likes to show numbers in 5 year time frames to make sure that accounting nuances fade away. If you break it down into these three 5-year frames, you can see the impressive results of Markel.

The insurance business raised its underwriting profit from 184m to 1777m, Markel Ventures EBITDA grew from 133m to 1710m and the investment income also increased significantly. At the same time Markel’s share price is only up 16% in the last 5 years.

Valuation Context:

Tom Gayner states very nicely in the 2022 shareholder letter, why the GAAP revenue numbers are a very flawed metric for Markel:

“Total revenues” include two distinct types of “revenues.” One type is the normal recurring revenues from each of our three engines of Insurance, Markel Ventures, and Investments. Our

insurance premiums and fee income streams are revenues, sales of the products and services in

Markel Ventures are revenues, and interest and dividend income from our investment portfolio are all revenues. That all makes sense to me. We also have some non-recurring revenues in our three engines, like the gains from the sale of our managing general

agent businesses this year. For the purposes of this discussion, let’s call all of those “orange revenues.”

The other component of “revenues”, according to GAAP, is the unrealized changes in the value of our equity portfolio. When stock markets decline, as they did in 2022, we report negative revenues from our equity holdings even if we didn’t sell anything. Changes in the market price of equities, positive or negative, flow through the line of “total revenues.” Let’s call those “blue revenues.”

I completely agree that we should report on our investment returns, but this strikes me as a curious way to describe them in our financial statements.

To me, it’s like talking about chocolate milk and motor oil. Both are fine substances. They both play critical roles in my life. They can both be measured in terms of fluid ounces. That said, I’ve never combined the two into one composite measurement"

“Total revenues” at a company with financial and non-financial businesses like Markel must combine these two disparate streams into one container labeled “total revenues” as mandated by GAAP accounting.

I would neither drink the contents of that container nor put it in my car’s engine. Therefore, I think it’s important to break things down into their separate components to help provide greater understanding.

Our “orange revenues” increased 21% to $13.2 billion in 2022 from $10.9 billion in 2021. That is an excellent result. It reflects the superb accomplishments of our associates from all around the world. That number describes how we served our

customers with products and services that they needed and wanted. That’s why we’re happy and proud of what took place in 2022.

Our “blue revenues” swung to a negative $1.6 billion in 2022 compared to positive $1.9 billion in 2021. This is not surprising. Equity markets experienced their worst decline since the 2008 financial crisis causing our portfolio of publicly-traded stocks to decline in 2022.

Over the last five years, we earned an annual return on our equity portfolio of 9.5% and over the last ten years, we earned an annual return of 13.2%.

In the shareholder letter Tom Gayner gives us his view on valuating Markel:

“If you were valuing a fruit tree, the value is the present value of the fruit the tree will produce over time. Same thing with our investment portfolio. As such, we simply take the total value of our investment portfolio and subtract out all debt, to get an indication of the value of the balance sheet part of Markel.

Another important part of estimating an indication of the value of Markel stems from the earnings power of our Insurance and Markel Ventures operations. We take the normal, annualized earnings from those operations and multiply that by a consistent and reasonable multiple year-by-year. That process provides an indication of the total value of Markel’s income statement. Then we add those two parts together to determine our own sense of what each share of Markel is worth.

We track that number every year. Since our initial public offering in 1986, that number correlates to the actual price of Markel stock over time. Sometimes the gap between the two lines is wider, sometimes it is narrower. Over time, both lines head in the same direction.”

Valuation

To properly valuate Markel, we need to break it down into 3 pieces:

Insurance (and Reinsurance)

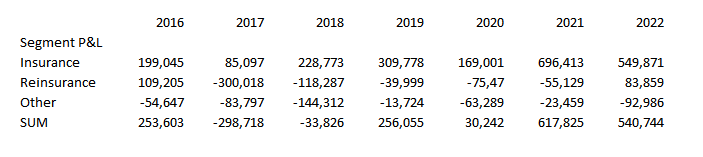

Taking the segment P&L from the annual report I have included all parts apart from Investing and Ventures. 2017 was a outlier with massive damages in the US from Hurricanes Harvey, Irma, Maria and Nate and the wildfires in California. Taking the average of the last 4 years, the (Re-)Insurance segment has an average P&L of 360m. per year.

This P&L is likely to rise due to a larger business and better interest rate environment for insurance companies.

Investment

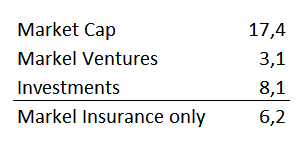

The current market value of the equity ownership is valued at 8.1bn. Given Markel’s great track record, that value is likely to change upwards even without any new investments.

Markel Ventures

With a twelve trailing month net income to shareholders of $206.2 million and the careful selection by Markel we can apply a very conservative 15x multiple to Markel Venture to arrive at a valuation. Applying a 15x multiple to the venture business gives us a valuation of 206.2m * 15 = 3.093bn or 3.1bn.

Sum of the Parts

With a market capitalization of $17.4bn at the time of writing, Markel has 8.1bn worth of equities (stocks) and the Markel Venture part can be valued at 3.1bn.

That gives us the valuation of the Insurance business.

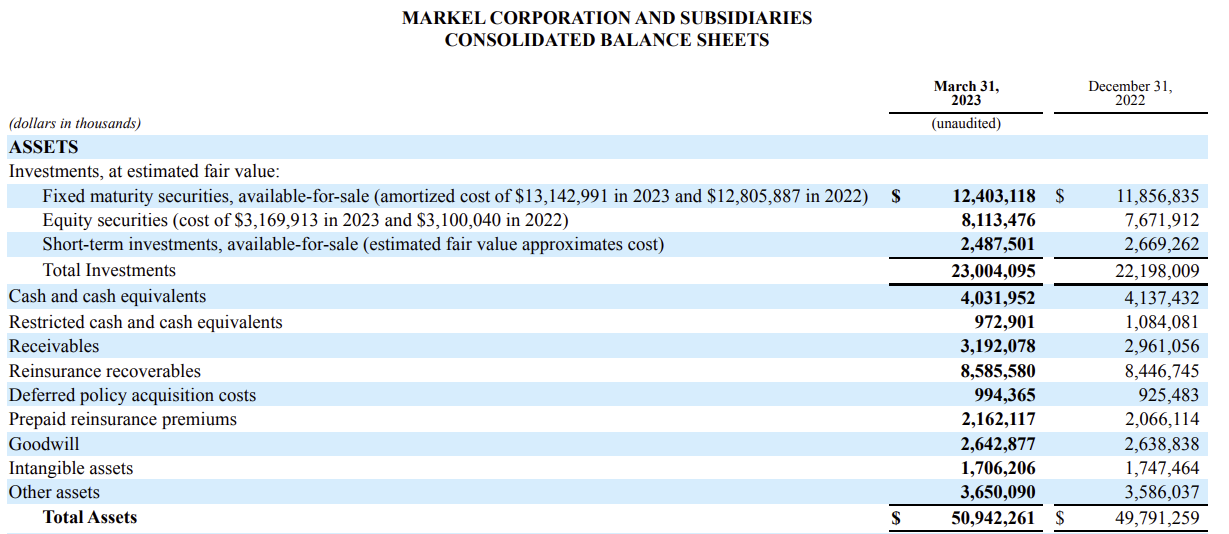

Considering that Markel owns 12.4bn in fixed maturity securities, 2.5bn in short-term investments and another 4bn in cash minus 3.9bn in long term debt we arrive at a net cash surplus of 15bn.

The stand alone insurance business is only valued at 6.2bn and it’s not the case, that Markel is losing a ton of money in the insurance business. Quite to the contrary, Markel is earning a handsome profit, which in turn it can invest in further equity purchases or additional companies for Markel Ventures. If we take the average of the last 4 years with a P&L of 360m, then the insurance business is valued at a multiple of 17.

Or if we take another approach:

Markels Investment assets + Cash equal 27bn. Long-term debt is 3.9bn. That makes roughly 23bn more assets than debt. The total market cap of Markel is 17.4bn.

You can buy right now a very interesting portfolio of assets with a great management team below the market value. This 27bn do not include the insurance business or Markel Ventures.

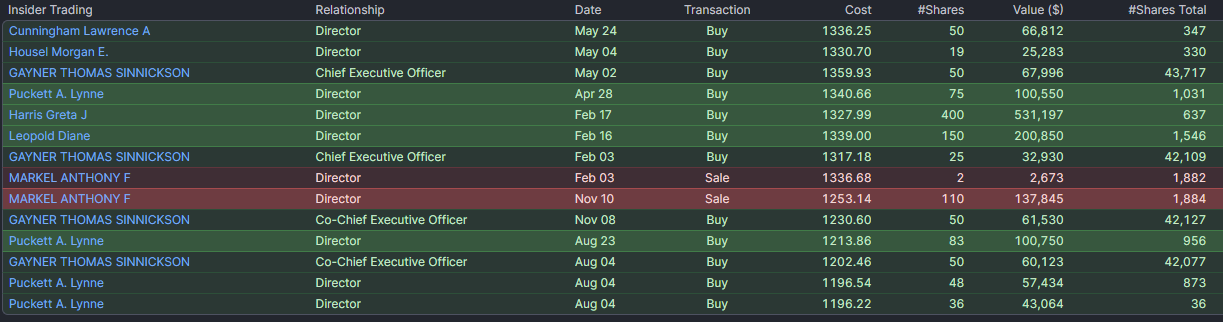

Management Trades

The absolute majority of recent insider tradings have been buys and CEO Tom Gayner said multiple times, that he believes the company is undervalued at the current price. Thankfully his actions follow his words.

Markel itself has been buying back shares in the last years and reduced the outstanding share count from 14m at the end of 2017 to 13.54m at the end of Q1/23.

Summary

Markel is a tough company to analyse as you can see outlined in this post. I believe that Markel is at a very attractive valuation at this point. Since roughly 2018 the shares went sideways and the company itself has shown tremendous growth and profitability. The rising interest rate environment will further fuel the returns for the bond holdings

If you read all the way to the end I would be more than happy if you subscribe to my substack and follow me on twitter: https://twitter.com/41investments

If you like this post, check out my previous deep dives on

Adobe: https://41investments.substack.com/p/adobe-fundamental-deep-dive

American Express: https://41investments.substack.com/p/american-express-deep-dive

Evolution: https://41investments.substack.com/p/evolution-ab-deep-dive

Expedia: https://41investments.substack.com/p/expedia-deep-dive

Fortinet: https://41investments.substack.com/p/fortinet-stock-analysis-and-deep

InMode: https://41investments.substack.com/p/inmode-deep-dive

Markel: https://41investments.substack.com/p/markel-deep-dive

MercadoLibre: https://41investments.substack.com/p/mercadolibre-deep-dive

Texas Pacific Land: https://41investments.substack.com/p/texas-pacific-land-deep-dive

British American Tobacco: https://41investments.substack.com/p/british-american-tobacco

Amadeus FiRe: https://41investments.substack.com/p/amadeus-fire-deep-dive

Datagroup: https://41investments.substack.com/p/datagroup-deep-dive

Invest at your own risk, this is not financial advice! This is not a recommendation to buy or sell securities discussed in the article.

41