British American Tobacco Stock Analysis & Deep Dive

Close to 40% FCF yield for a non-software company

Intro

While my main focus is on software and tech companies, every now and then there is a company from another sector that gains my interest. In this case, it is a tobacco company with an FCF margin in the high 30s. That is usually only reached by software companies.

The Company

British American Tobacco was established in 1902 and is by sales the largest tobacco company in the world. The company was born through a joint venture of Imperial Tobacco of England and American Tobacco from the US. It is headquartered in London, England but also trades on the NYSE with the ticker BTI (I will refer to the company as BTI from here onward). More than 50000 employees run the operations in more than 180 countries.

BTI has a history of takeovers with smaller ones such as Turkey's state-owned cigarette maker Tekel in 2008, Indonesia’s Bentoel Group in 2009, Colombian Productora Tabacalera de Colombia in 2011, and Croatian TDR d.o.o. Brands and Factory in 2015. The largest takeover was Reynolds American. In 2004 BTI acquired a 42% share and bought the remaining share in 2017 of $49.4bn. This brought brands such as Newport, Lucky Strik,e, and Pall Mall to the BTI portfolio.

Formula 1 banned tobacco advertising in 2006, but since 2019 BTI and McLaren are partners and BTI is the main sponsor. BTI uses the space to advertise Vuse, its fastest-growing brand.

The Industry

The global tobacco industry is estimated to be worth $935bn. With 83% of the total value of tobacco sales worldwide, traditional cigarettes dominate the market and over 2.8 billion cigarettes are consumed yearly (excl. China). Worldwide 18% of adults are smoking. Even though the cigarette market is in a slight decline, the growth in next-gen products provides overall growth for the tobacco market with a CAGR of 3.4% until 2030.

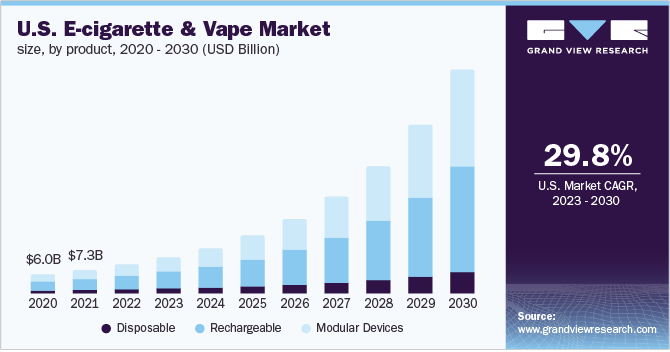

The global vapour market is estimated to $55bn. BTI defines vapour as: “Vapour products are battery-powered devices that heat liquid formulations – e-liquids – to create a vapour which is inhaled”. E-cigarettes and Vaping products are expanding rapidly. For the US a CAGR of 30% is estimated until 2030.

Citi had some interesting points about the global nicotine market. I’ve highlighted those below

Some words on the ESG nonsense: Personally I find it a bit odd, that selling harmful products (I know they are less harmful than combustibles) is seen as a positive factor for a good ESG score. This shows again that the whole ESG debate is sometimes quite fruitless.

The Business

In software, we love reoccurring revenues. What kind of better customer is there, than the one who is addicted to your product? Welcome to the world of tobacco, a world where the health hazards have been known for decades and the customers keep on coming back. You can argue that this is as great a business model as software subscriptions.

45% of the group’s revenue comes from the US, 15% from the rest of the Americas + Africa, 23% from Europe, and 16% from Asia and the Middle East. 83% of BTI revenues come from traditional cigarettes, while 10% are from new categories. The rest is split between traditional oral tobacco and others.

As one expects, tobacco is a highly profitable business. With a 9% CAGR on EPS and a 6% CAGR on dividends, BTI has a strong track record over the last 10 years.

Divestment of former markets continues to be expensive for BTI. The disposal of the Iranian businesses cost BTI £358m, whereas the transfer of the Russian and Belarusian businesses costs £612m.

This graph gives a good overview of the product portfolio of BTI. BTI really makes an effort to promote its new products and is one of the very few companies that always positions its cash cow (traditional cigarettes) at the very bottom of the list.

BTI is leading the vaping industry with a 41% market share from Vuse in 2022. This share has grown from only 25% in 2020. In terms of hardware, Vuse is leading the market with a 64% volume share, which is a good indicator for future growth. On top of that the margins of vaping products are even better than cigarettes. The US, UK, France, Germany, and Canada make up 88% of the vapour revenues.

Vaping and THP are even more profitable than cigarettes: “So, take the example of Poland for example where margins are almost five times higher in THP than they are in Combustibles when you compare our own portfolio of cigarettes, and we migrate to our products in THP.”

If you want to read the full article and learn about the management, the composition of the segments, takeovers, risks, fundamental analysis, and a conclusion please subscribe and support my work. To all existing subscribers: Thank you for your support and enjoy the rest of the article!

Keep reading with a 7-day free trial

Subscribe to 41investments’s Substack to keep reading this post and get 7 days of free access to the full post archives.