Texas Pacific Land Stock Analysis & Deep Dive

Let's play Monopoly and start with the best lots

Intro

With the booming oil industry in Texas and Warren Buffett's continuous buying of Occidental Petroleum, I searched for ways to profit from the boom in the Permian Basin. Texas Pacific Land (TPL) is one of the purest plays available for the Permian Basin and refers to itself as the ETF of the Permian Basin.

The Company

In 1871 The Texas & Pacific Railway was created and the state of Texas gave 3.5m acres (ca. 14.000 square kilometers) of land to start the company. When the Texas & Pacific Railway filed for bankruptcy, all the land assets were placed in the Texas Pacific Land Trust to have a safe place. More than a century later this makes TPL one of the largest landowners in the state of Texas. In 2017 the management of TPL made the active decision to become an active corporation vs continuing as a passive trust as it has been in the previous 100+ years. This led to an increase in CapEx to start and enlarge the water business. Due to the new structure of the company, the name was changed from Texas Pacific Land Trust to Texas Pacific Land Corporation.

This is one of their remaining steam locomotives.

Not known at the time of the creation of the trust were the great oil & gas reserves which are located on the lands now owned by TPL. This makes the land incredibly valuable. Today TPL owns 874k surface acres of land (3.5k square kilometers) in West Texas of which the vast majority is based in the Permian Basin. On top of that, TPL has royalty rights in an additional 460k acres (1.8k square KM).

TPL makes money through royalties from oil, water, and surface rights. What makes TPL special is the fact that the company owns the land and therefore the assets and resources both on the surface and below the earth. At the same time, TPL does not participate in the high CapEx necessary business of actually developing and operating the oil wells.

TPL had revenues of $667m in 2022 with only 100 employees. This makes for a crazy revenue ratio of $6.7m per employee

The Industry

Oil is still driving the world and overall oil demand keeps rising. Thanks to the advances in new drilling methods such as fracking, the US overtook Saudi Arabia and Russia in 2017 as the largest producer of oil in the world. Most of this additional supply of oil is coming from the Permian basin, in which TPL coincidentally owns large pieces of land.

The Permian basin is located mostly in Texas and also covers some parts of New Mexico.

The first well in the Permian Basin was drilled in 1920. In 1970 gas output reached a peak of 10bn cubic feet per day and 2m barrels of oil. Output fell sharply by more than 60% until the mid-2000s. With the rise of horizontal drilling and fracking the output of the Permian basin has skyrocketed.

The attack of Russia on Ukraine led to a strong price increase in both gas & oil. The price for WTI reached more than 100$ a barrel for the first time since 2014. This increase in the oil price led to increased drilling in the Permian Basin of which TPL benefits strongly. The Permian Basin accounts for an ever-increasing share of the overall US oil and gas production.

If you are interested in how fracking works, I can highly recommend this video. You will also see why TPL is expanding into the water side of the business. Loads of water are used in the process and TPL is happy to provide their customers with it.

The Business

Writing a deep dive takes me 40+ hours to get a proper understanding of the company and the attributes of the industry it is working in. You will support me a great deal if you a) subscribe to this substack and b) recommend this blog to your friends and family. To all existing subscribers: Thank you for your support! :)

TPL takes an average of 4.4% of the oil revenue that is being produced on their land which contributes 68% of overall TPL revenue. TPWR (Texas Pacific Water Resources) contributes 24% of the overall revenue, while SLEM which is defined as TPL’s cumulative easements and other surface-related income adds the remaining 8% of overall revenue. Every now and then TPL sells a small piece of the owned land, which increases revenues as a one-time effect in the period.

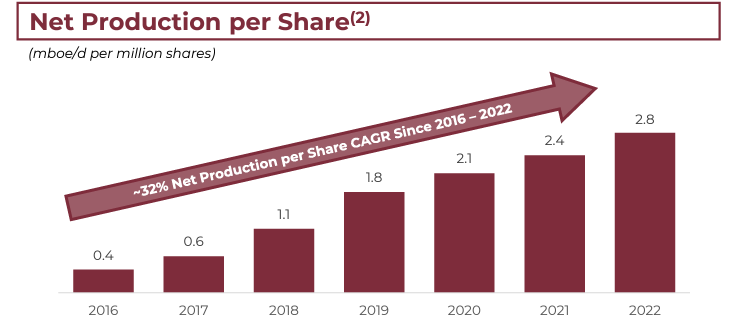

Net production of thousand barrels of oil equivalent per day (mboe/d) has been increasing steadily for TPL. This effect is a great hedge against falling or flat oil prices since the increase in volume will make up some of the losses.

The easements (the right of use for a defined piece of land) come in many different forms. These include oil, gas, and water pipelines, roads as well as land for solar farms. These easements are signed for 30 years and are renewed every 10 years with an additional payment. TPL estimates that the easements have great potential to become a major revenue contributor in the long term.

If you want to read the full article and learn about the management, the composition of the segments, takeovers, risks, fundamental analysis, and a conclusion please subscribe and support my work. To all existing subscribers: Thank you for your support and enjoy the rest of the article!

Keep reading with a 7-day free trial

Subscribe to 41investments’s Substack to keep reading this post and get 7 days of free access to the full post archives.